The first three parts of this series traced the consumer’s pain, the trade’s defensive pivot, and the emerging global marketing playbook in a market defined by declining volume, premiumization, and demographic turnover. This final roadmap distills those forces into an executive action plan: move from a “Prestige” mindset to a “Utility” framework or risk aging out with your oldest customers.

Phase 1: Economic Realignment

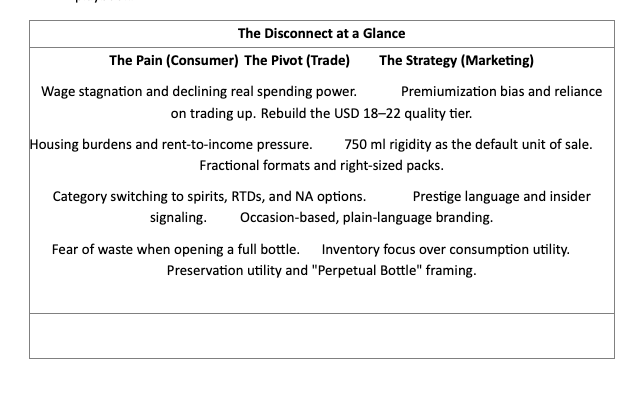

- Rebuild the “On-Ramp” (USD 18–22)

Premiumization boosted top tiers but hollowed out the everyday table wine segment just below them, where younger and middle-income consumers used to onboard into the category. Wineries must rebuild a credible quality tier in the USD 18–22 range to capture the “Daily Drinker” who still wants wine but will switch categories when value feels out of sync with rent, groceries, and student loans. Goal: Create a high-value, low-risk entry point that does not require a “luxury” budget or specialized knowledge to justify the spend. - Solve the “Rent-to-Wine” Ratio

For Millennials and Gen Z, housing costs are not a backdrop; they are the main character. Three-in-five Gen Z renters are rent-burdened, with Millennials not far behind, compressing discretionary spend on categories like wine even as list prices continue to rise.

Action: Direct-to-consumer (DTC) models should lean into “subscription flexibility” (pause/skip months, smaller clubs, mixed-format options) and “shared shipping” or pickup partnerships to lower the perceived fixed cost of staying in the wine habit for urban, rent-burdened drinkers.

Phase 2: Format & Utility Innovation

3. The Fractional Revolution

The 750 ml bottle is a legacy format optimized for shared, sit-down occasions—exactly what many younger drinkers have less of. As solo consumption, small households, and “one nice glass” occasions rise, a full bottle increasingly feels like too much commitment in both price and waste risk.

Action: Transition at least 25 percent of production to fractional formats, 375 ml bottles, premium 250 ml cans, or multi-pack minis, to match modern consumption patterns without diluting brand equity.

Outcome: Reduces the “financial commitment” per occasion, lowers “fear of waste,” and positions wine as a flexible, right-sized option instead of an all-or-nothing bottle.

4. Weaponize Preservation

If consumers are drinking less per occasion, the perceived perishability of an opened bottle becomes a psychological tax on wine that spirits simply do not pay. Most households still lack good preservation tools, which reinforces the idea that wine must be finished or wasted within a night or two.

Action: Include high-quality stoppers or vacuum systems with case purchases or club tiers, and communicate simple preservation rituals as part of the brand story.

Outcome: Reframes wine from a “perishable expense” to a “durable asset” that can be enjoyed over several days, narrowing the perceived utility gap versus spirits and RTDs.

Phase 3: Communication & Branding

5. Pivot to “Occasion” Messaging

The old story, terroir, soil types, clonal selections, still matters to insiders but does not answer the real question for younger, time-poor buyers: “When do I open this and with what?” Occasion-led cues reduce friction, shrink choice overload, and make wine feel like an intuitive fit for everyday micro-moments, not just special-occasion dinners.

Action: Replace or complement technical back-labels with occasion-based descriptors such as “Perfect for Tuesday Takeout,” “Rooftop Sundowner,” or “Friendsgiving Red,” and mirror that language across e-commerce filters and shelf talkers.

6. Radical Transparency

Health, wellness, and ethics now sit in the same consideration set as flavor and price for Millennials and Gen Z. At the same time, broader packaged-goods regulation and retailer expectations are pushing toward more explicit disclosure of ingredients, calories, and sugar.

Action: Implement “Clean Labeling”—ingredients, calorie counts, sugar levels, and, where appropriate, farming or sustainability certifications—in both physical and digital touchpoints.

Outcome: Converts skepticism into trust, aligns wine with the transparency norms of other food-and-beverage categories, and makes it easier for moderation-minded consumers to keep wine in their repertoire instead of switching to RTDs or NA options.

Phase 4: Competitive Positioning

7. Combat the “Efficiency of the Buzz”

Spirits and RTDs are winning share not only on flavor and convenience but on what might be called the “efficiency of the buzz”: higher perceived payoff per dollar and per calorie. As Gen Z and Millennials experiment with “less but better,” tequila RTDs, canned cocktails, and hard seltzers offer frictionless entry points where wine often still feels slow and formal.

Action: Reposition wine as the superior choice for ritual, food-pairing, and social connection, leaning into slower, more intentional occasions where the value is in the experience, not just ABV throughput.

8. Lower the “Risk Premium”

For many emerging consumers, wine still feels like an exam they did not study for: too many SKUs, opaque labels, and a fear of “getting it wrong” at the table or in the cart. Traditional critic scores increasingly resonate with older cohorts, while younger buyers trust peers, aggregated ratings, and flavor-based recommendation engines.

Action: Use data and social proof—peer reviews, crowd-sourced flavor maps, “people who liked this also enjoyed…” prompts—to reduce the perceived risk of trial, especially in the rebuilt USD 18–22 segment.

Outcome: Lowers the psychological barrier to exploration and makes wine feel as navigable as other algorithm-assisted categories like streaming and e-commerce.

Phase 5: Long-Term Sustainability

9. Demystify the Gatekeeping

Several recent industry reports converge on a common diagnosis: wine’s insider culture often makes new consumers feel “small” or excluded instead of welcomed. The result is a category that over-serves aficionados while under-serving curious, high-potential newcomers who might otherwise grow into loyal buyers.

Action: Simplify the buying experience across retail, DTC, and hospitality—fewer hierarchical cues, more intuitive filters (taste, mood, occasion), and staff training that prioritizes psychological safety over performance tasting notes.

Goal: Shift decision-making from “System 2” (effortful decoding) to “System 1” (fast, intuitive recognition) so consumers can choose confidently without a crash course in appellations and vintages.

10. Invest in the “New Floor”

Boomers and older Gen X consumers still anchor premium revenues but are no longer a growth engine; their consumption is flat to declining in both volume and frequency. At the same time, Millennials have become the largest U.S. wine-consuming cohort by headcount, while Gen Z is slowly—but selectively—entering the category amid more category competition than any previous generation faced.

Action: Reallocate roughly 30 percent of marketing and innovation spend away from “legacy collectors” and into “first-time explorers,” using formats, price points, and stories that meet younger consumers on their terms rather than asking them to inherit the old playbook.

References

Anderson, K., & Pinilla, V. (2023). Annual database of global wine markets, 1835–2022. Wine Economics Research Centre, University of Adelaide. https://economics.adelaide.edu.au/wine-economics/databaseseconomics.adelaide+1

Anderson, K., & Pinilla, V. (2025). The Global Wine Markets Annual Database, 1835–2023. IVES Technical Reviews. https://ives-technicalreviews.eu/article/view/8047/35396ives-technicalreviews+1

Bank of America Institute (2025). Raising the bar or last call? Consumer Morsel on drinking trends. https://institute.bankofamerica.com/content/dam/economic-insights/consumer-morsel-drinking-trends.pdf[institute.bankofamerica]

Beverage Alcohol Growth Comes from Meeting Consumers in Their Moments (2026). LinkedIn / Bevgenie. https://www.linkedin.com/posts/bevgenie_this-quote-from-nielseniqs-2025-beverage-activity-7419748145812713472-1ZLe[linkedin]

Bureau of Labor Statistics (2026). Consumer Price Index Summary – December 2025. https://www.bls.gov/news.release/cpi.nr0.htm[bls]

Bureau of Labor Statistics (2026). Consumer Price Index: 2025 in review. https://www.bls.gov/opub/ted/2026/consumer-price-index-2025-in-review.htm[bls]

CEIC Data (2025). United States CPI: Food and non-alcoholic beverage change. https://www.ceicdata.com/en/indicator/united-states/cpi-food-and-non-alcoholic-beverage-change[ceicdata]

Decanter (2024). Can the wine industry adapt to the “lifestyle generations”? https://www.decanter.com/wine-news/can-the-wine-industry-adapt-to-the-lifestyle-generations-524654/[decanter]

Einar Willumsen (2025). RTD Alcohol Trends: Top Trends in the Ready To Drink Market 2025. https://einarwillumsen.com/news/rtd-alcohol-trends/[einarwillumsen]

Food & Wine (2025). How Gen Z is quietly rewriting the rules of wine. https://www.foodandwine.com/gen-z-wine-trends-2025-11868702[foodandwine]

NIQ (2025). Trends and Disruption in Beer, Wine, Spirits & Beyond. https://ecrm.marketgate.com/MarketingFiles/Media/20250917/NIQ_Beverage_Alcohol_Presentation.pdf[ecrm.marketgate]

NIQ / NielsenIQ (2025). The Fourth Category: A Mid-Year Update on Ready to Drinks. https://nielseniq.com/global/en/insights/report/2025/the-fourth-category-a-mid-year-update-on-beverage-alcohol/[nielseniq]

OhBev (2026). U.S. wine market forecasts and trends. https://www.ohbev.com/blog/us-wine-market-2024—trends-and-opportunities-and-beyond[ohbev]

Silicon Valley Bank (2026). State of the U.S. Wine Industry (25th edition). Coverage via: Wine Enthusiast and PR Newswire. https://www.wineenthusiast.com/culture/industry-news/svb-state-of-wine-industry-report-2026/; https://www.prnewswire.com/news-releases/silicon-valley-bank-releases-25th-annual-state-of-the-us-wine-industry-report-302661928.htmlprnewswire+1

The Drinks Business (2026). Top findings from the SVB Wine Report. https://www.thedrinksbusiness.com/2026/01/top-5-findings-from-the-svb-wine-report/[thedrinksbusiness]

Wine Business Monthly (2026). Outlook & Trends: Embracing the Correction and Staying Relevant. https://www.winebusiness.com/wbm/article/312710[winebusiness]

Wine Market Council / Thach, L. (2025). 2025 Annual Meeting insights: How Gen Z, diverse consumers, and DTC trends are reshaping wine. https://grapeandwinemag.com/2025/07/13/wine-market-council-2025-annual-meeting-insights-how-gen-z-diverse-consumers-and-dtc-tren/[grapeandwinemag]

Wine popularity ebbs and flows among generations (2026). Beverage Industry. https://www.bevindustry.com/articles/98112-wine-popularity-ebbs-and-flows-among-generations[bevindustry]

WineNews (2026). Impact of duties and new consumers to be intercepted – 2026 forecasts of U.S. wine market. https://winenews.it/en/impact-of-duties-and-new-consumers-to-be-intercepted-2026-forecasts-of-us-wine-market_579517/[winenews]

Yahoo Finance (2025). 3 challenges the wine industry faces in 2026. https://finance.yahoo.com/video/3-challenges-wine-industry-faces-215708281.html[finance.yahoo]

Yahoo Finance (2025). Is premiumisation where the growth lies for wine? https://finance.yahoo.com/news/premiumisation-where-growth-lies-wine-130025027.html[finance.yahoo]

Zillow (2024). 3 in 5 Gen Z renters are rent burdened, but Millennials had it worse. https://zillow.mediaroom.com/2024-10-22-3-in-5-Gen-Z-renters-are-rent-burdened,-but-Millennials-had-it-worse[zillow.mediaroom]

Zillow (2024). Zillow Rentals Consumer Housing Trends Report 2024. https://www.zillowstatic.com/bedrock/app/uploads/sites/42/2023/11/Zillow-Rentals-Consumer-Housing-Trends-Report-2024.pdf[zillowstatic]

Zillow (2025). Renters need to earn over USD 80K to afford a typical apartment. https://www.multifamilyexecutive.com/property-management/rent-trends/renters-need-to-earn-over-80k-to-afford-typical-apartment-zillow[multifamilyexecutive]

© 2026 Dr. Elinor Garely / InMyPersonalOpinion.Life Protected by U.S. & international copyright + DMCA. No reproduction, reposting, redistribution, adaptation, or AI training allowed. Brief quotes only with full credit + link. Permissions: EG@InMyPersonalOpinion.Life000

000